.png)

Market Update

Bitcoin ETF flows appear to have stabilised after three months of outflows totalling roughly US$50B. This is a constructive sign that the corrective phase may be nearing an end, though we can’t be certain.

The current bitcoin price drawdown of 31% is modest compared to prior cycles, which have seen drawdowns of 75% or greater. A silver lining is that the asset class continues to mature, with bitcoin forming higher lows over time.

It’s now almost three months since we saw an all-time high of approximately US$126k on October 6. What followed on October 10 was the largest liquidation wipe-out in crypto’s history, as leveraged investors (predominantly longs) lost approximately US$19B in a 24-hour period.

We believe the October 10 liquidation event has dampened investor appetite, compounded by the investment spotlight shifting towards the ongoing AI revolution. At the same time, foreign central banks have continued reducing exposure to US Treasuries and dollar reserves in favour of gold, contributing to strong precious metals performance over the last year.

Historically, the most durable crypto recoveries have followed forced deleveraging events like October 10, where excess leverage is cleared, weak hands exit, and price discovery resets on a healthier footing.

Encouragingly, long-term bitcoin holders have recently turned into positive net accumulators for the first time since July 2025, adding approximately 33,000 BTC over the last 30 days. This suggests momentum may be starting to return.

Speaking more broadly across the asset class, it’s increasingly clear that sticking to quality in crypto matters even more than in equities. Tokens without network effects, revenues, or clear product-market fit are down between 50% and 90% from all-time highs, and the speculative fervour of prior cycles has not materialised this time around.

We see this as a positive development, and our investment thesis remains aligned with being heavily weighted towards blockchains that demonstrate durable moats and long-term adoption.

Outside of bitcoin, we continue to take a favourable view on ethereum, which underpins the majority of the approximately US$300B stablecoin market and around 65% of non-stablecoin real-world assets currently being tokenised.

A recent example is JP Morgan, the world’s largest GSIB (globally systemically important bank), which has joined the likes of BlackRock in launching its first tokenised money market fund, leveraging ethereum as the platform to tokenise the fund and provide yield directly to investors’ wallets.

Events like these are a big deal. Over the long term, we expect trillions of dollars’ worth of assets to move on-chain, generating fees for these networks and potential upside for token holders.

While corrective phases in crypto are never enjoyable, we believe that this too shall pass.

Constructive catalysts on the horizon include the potential for further US rate cuts, improving global liquidity conditions, and increasing levels of institutional adoption as more capital moves on-chain.

The spiralling US$38T US federal debt burden remains difficult to address without significant cuts to essential services. At current interest rates, annual interest expense is approaching US$1.2T, now exceeding spending on defence, education, and Medicare individually.

This persistent deficit underpins our long-term constructive investment thesis for neutral and alternative stores of value outside the US dollar, such as bitcoin and ether.

That said, there are headwinds to monitor.

US unemployment is continuing to rise, alongside increasing political and social division, which may complicate the passage of further pro-crypto legislation as we approach the US mid-term elections in November 2026.

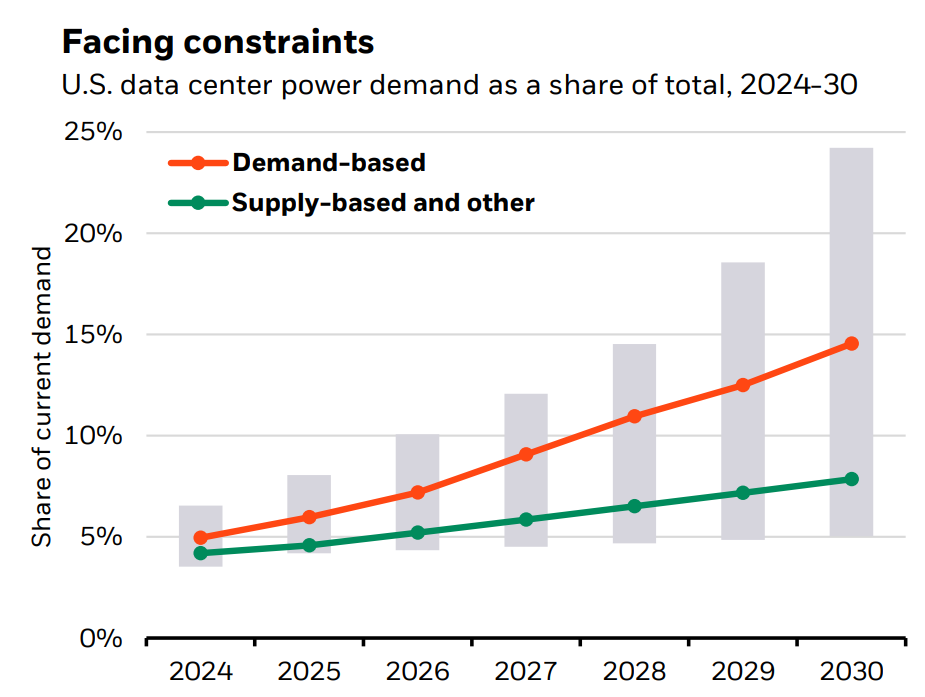

Another tail risk would be a sharp slowdown in AI-related investment. Should the AI boom fizzle and capital expenditure from major hyperscalers decline materially, a risk-off move in equities could spill over into crypto markets.

However, we see this as a less likely scenario. Demand for data centres and advanced chips remains strong, while large technology firms remain well capitalised and increasingly able to access private credit markets to fund ongoing capital expenditure.

Should you have any questions or like to discuss our views on the market - reach out anytime.

Wishing you a prosperous 2026.

James

James Brannan

Managing Director

BlockByte