.png)

Executive Summary

- Over the last 10 years, Bitcoin has provided the best risk adjusted return across asset classes and is not yet widely held by the majority of investors, presenting an asymmetric opportunity.

- Inflation remains stubbornly high, those most impacted are everyday citizens that lack financial education, have low incomes and don’t own assets.

- The driver of inflation has been irresponsible actions by governments and central banks but this is still largely unrecognised and poorly understood by the general population.

- The world’s leading economy, the US, has reached an inflection point where record debt levels, high inflation and ongoing government deficit spending may lead to prolonged inflation and the risk of debt spiraling out of control.

- To manage risks against ongoing debasement and rising debt levels, investors should consider an allocation to scarce, desirable assets – like bitcoin.

- In addition to the launch of the ETFs driving significant demand, the upcoming bitcoin halving will reduce potential sell pressure by ~$11.5B over the course of the year or ~450 bitcoin per day, creating a net positive impact on price assuming demand remains similar.

Full Article

Much of the western world may have entered a new era, one where inflation becomes a more painful thorn in the foot for many.

Put simply, inflation occurs when demand exceeds supply for goods and services, pushing prices higher.

The COVID pandemic led to a surge in inflation due to stimulus support to help people and businesses get through a tough period and pay their bills. What often goes unrecognised is the history of rising debt that major economies like the US have been accumulating, and the impact this can have on long-term financial stability.

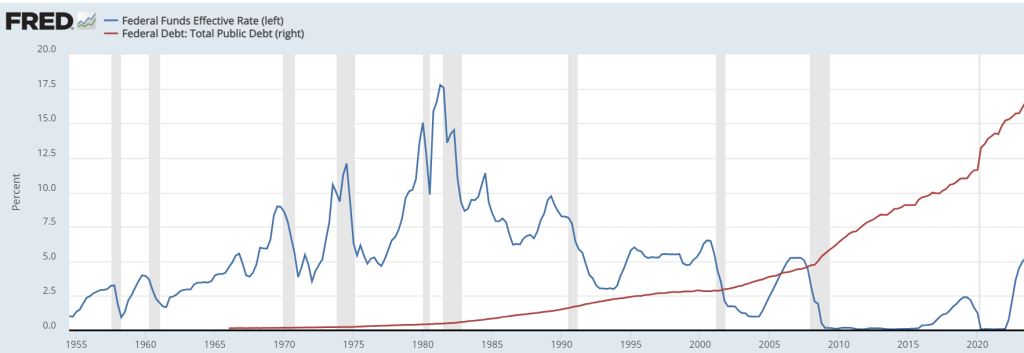

Since the 1980s, the US has increased public debts from ~$1 trillion to ~$35 trillion today (see the red line on the chart below). During this period, the Federal Reserve has been reducing interest rates to offset the impacts of rising debt and to continually stimulate growth in the economy (see the general downtrend of the blue line from 1980 to today).

When interest rates are low and the economy is flush with cash, people pay more for houses, consume more goods and services, and ultimately drive prices higher. Whilst some supply bottlenecks have been alleviated, additional drivers of inflation include significant spending on green infrastructure, global re-militarisation and rising costs of healthcare for aging populations.

Here’s a quote from Jamie Dimon’s recent annual letter:

“It is important to note that the economy is being fuelled by large amounts of government deficit spending and past stimulus. There is also a growing need for increased spending as we continue transitioning to a greener economy, restructuring global supply chains, boosting military expenditure and battling rising healthcare costs. This may lead to stickier inflation and higher rates than markets expect.” - Jamie Dimon's April 2024 Annual Letter. JP Morgan

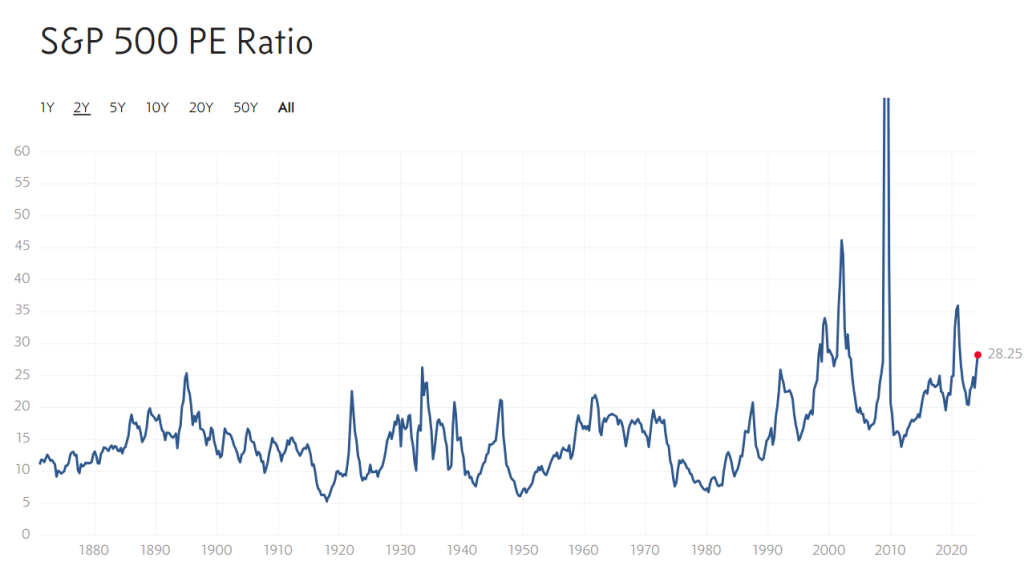

Whilst simply buying and holding traditional assets like property and the magnificent 7 stocks has been the trade of the last decade, many areas of the market have reached excessive valuation multiples on a historical basis.

Currently, the average price to earnings ratio of the S&P500 is 28, and the historical average is 16. That’s not to say these areas of the market won’t continue to perform well, but investors should be cautious when allocating to already heavily invested areas of the market.

Gold has traditionally been the safe haven for investors during times of high inflation. Indeed, gold is up 18% in the last year. However, gold investors should be aware that as prices rise, the supply of gold increases as miners expand exploration for gold, eventually dampening the price by increasing supply. Moreover, over a period of 10 years, the compound annual return of ~6% has not satisfactorily kept pace with inflation and markets as a whole.

Bitcoin presents investors with an asymmetric hedge against inflation. With the price only recently having broken record all-time highs, there is the addition of the halving expected on the 19th of April 2024, which will see the block rewards for bitcoin mining cut in half from ~900 bitcoin per day to ~450 bitcoin per day. At current prices of ~$70,000 USD, this will mean that the new daily supply of bitcoin entering the market will be cut from $63M per day before the halving to $31.5M per day. Over the course of a year this is ~$11.5B less in potential sell pressure from bitcoin miners.

In addition, we are seeing unprecedented demand for the bitcoin ETFs with volumes achieving net inflows of >$400M per day and 2 of the 9 ETFs already the most successful ETFs by inflows in the first 50 days compared to any other ETF in history. Both Blackrock and Fidelity now each individually hold more than $10B in bitcoin.

In closing, the vast majority of investors have yet to allocate to bitcoin, however, this is changing rapidly. I don’t think it’s wise to be too deterministic on what the future holds, but we should be prepared for all possibilities. This means holding a diversified portfolio, and as part of that portfolio mix bitcoin may have an increasingly significant role to play in hedging against inflation.